The five structural forces shaping 2026; economic divergence, AI acceleration, climate costs, trade pressures, and labor market changes, will directly reshape how consumers spend, save, and prioritize purchases.

Spending growth will become increasingly uneven. Households in the top income quartile are projected to increase spending by approximately 6.4%, supported by wage gains in high-skill sectors and stronger asset performance. In contrast, the bottom income quartile is expected to grow spending by just 1.8%, with many households effectively experiencing flat or negative real growth after inflation. This widening gap reinforces a two-speed consumer economy.

Value-seeking behavior will intensify. Private label and store brands are projected to reach 34% market share as consumers prioritize affordability in essentials such as groceries, household goods, and personal care. Discount retailers and bulk formats will gain share, particularly among middle- and lower-income households seeking cost control.

At the same time, premium and “affordable luxury” categories will continue expanding. Higher-income consumers are expected to increase spending on travel, dining, wellness, beauty, and subscription-based services. Rather than broad-based discretionary expansion, spending will concentrate in categories that deliver perceived quality, experience, or status.

Digital commerce will continue its structural rise. E-commerce penetration is projected to reach 28% of total retail sales, driven by convenience and improved price transparency. Artificial intelligence–powered personalization will influence approximately 84% of digital shoppers through product recommendations, dynamic pricing, and predictive marketing, raising conversion rates and deepening customer targeting.

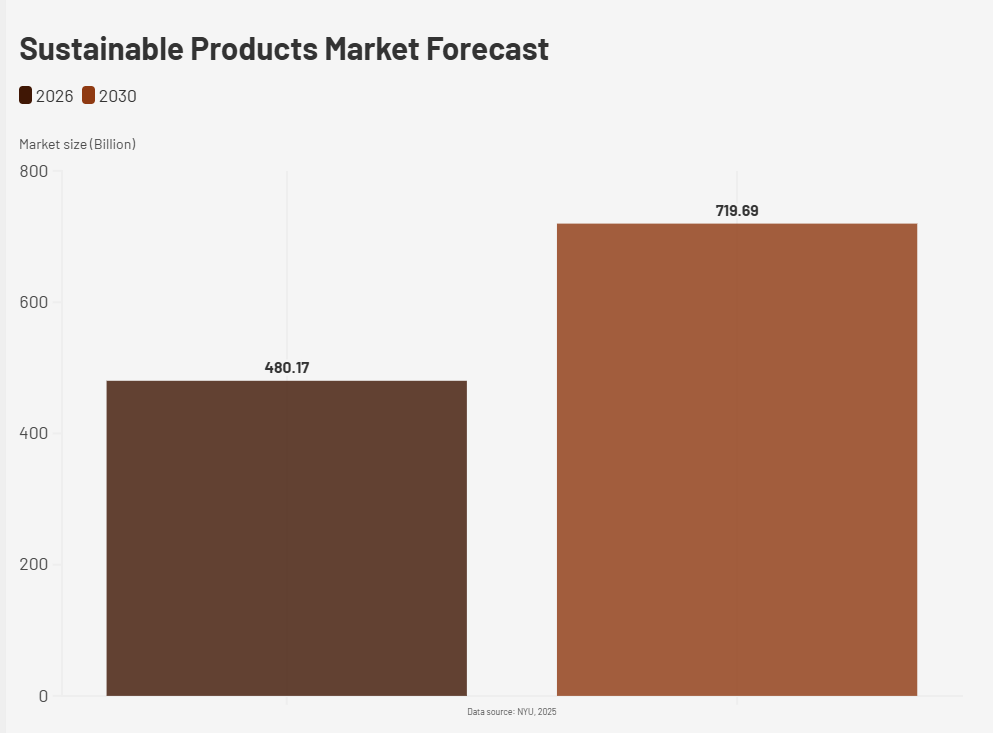

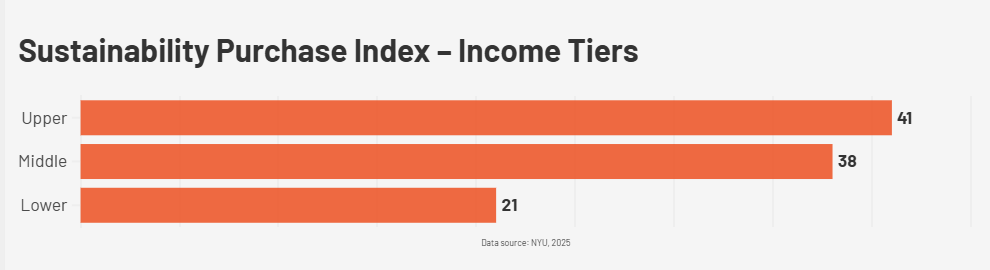

Sustainability preferences will stabilize rather than accelerate. Consumers are expected to tolerate price premiums of roughly 10–12% for sustainable products, but willingness to pay beyond that threshold will remain limited. This suggests sustainability is becoming an expectation in some categories, yet price sensitivity continues to constrain mass adoption.

The overall result is a strengthening barbell structure in the economy: premium and discount segments gain momentum, while the traditional middle market faces compression. Businesses positioned clearly at either end of the value spectrum are likely to outperform those competing on undifferentiated mid-tier offerings